The Upgrade That Wasn't: Q1 GDP, May PCE, and the Numbers Beneath the Numbers

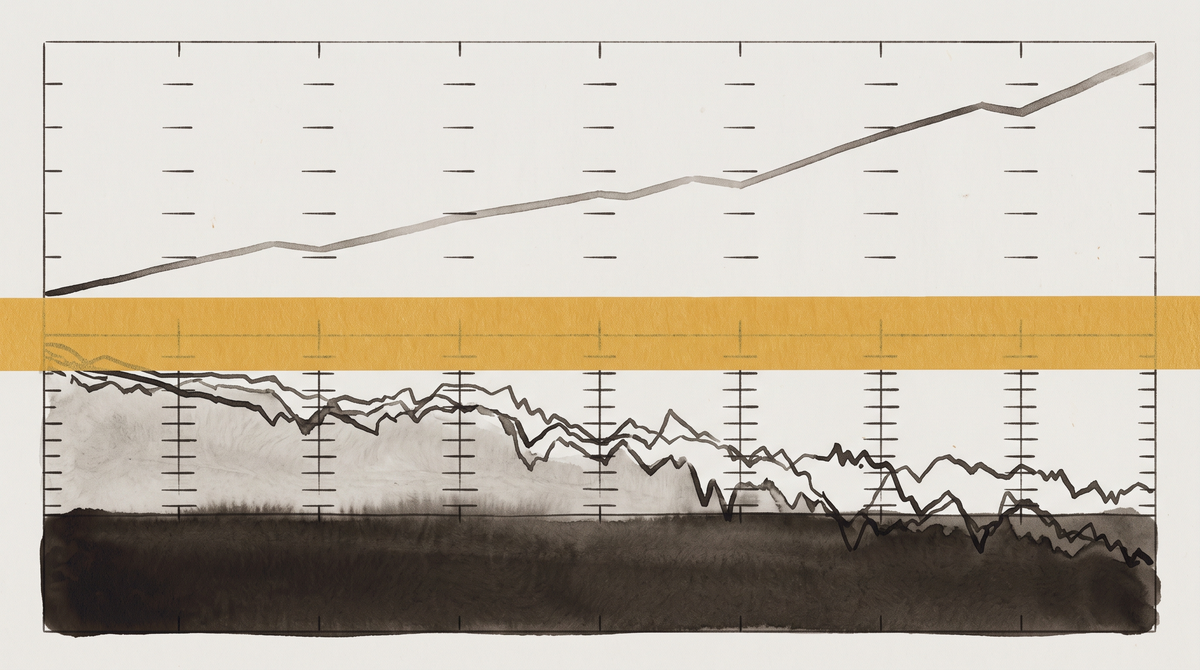

Q1 GDP was revised up to 2.1% on June 25 — but the upgrade came from a lower import figure, not stronger domestic demand. Consumer spending was simultaneously downgraded to 0.5%, the slowest since 2022. May PCE hit 4.1%, a three-year high.

The headline from June 25 was easy to write: the U.S. economy grew 2.1% in the first quarter. That's up from 1.6% in the prior estimate and looks like good news. What the coverage mostly skipped was where the upgrade came from — and what happened to private domestic demand in the same revision.

On June 25, the Bureau of Economic Analysis published two things simultaneously. The third estimate of Q1 2026 GDP revised the headline number up half a point, to 2.1%. At the same moment, the BEA released the Personal Income and Outlays report for May 2026, containing the month's PCE inflation reading. The GDP revision read as good news. The inflation data did not. The relationship between the two is what the standard coverage missed.

How GDP grew 2.1% without the economy getting stronger

The technical detail is critical: the 0.5-point upgrade to Q1 GDP was primarily driven by a downward revision to imports, not by stronger domestic economic activity. In GDP accounting, imports are subtracted — they represent spending on goods produced elsewhere. When imports are revised lower, GDP goes up even if nothing else in the domestic economy changed.

The meaningful question, then, is what happened to domestic demand. The BEA provides a measure for this: real final sales to private domestic purchasers, the sum of consumer spending and gross private fixed investment. In the second estimate, this figure was 2.4%. In the third estimate, it was revised down to 1.7% — a 0.7-percentage-point downgrade in the same release that produced the GDP headline upgrade.

The headline and the underlying measure moved in opposite directions.

Consumer spending — personal consumption expenditures — was revised to 0.5% annualized growth in Q1. That is the slowest quarterly rate of consumer spending growth since Q1 2022. The revision reflected decreased household spending on financial services and insurance. The American Bankers Association, in its DataBank analysis of the release, noted that the economy was becoming more reliant on non-residential investment than on consumer spending or housing — a composition shift that matters for durability.

Real Gross Domestic Income — GDI, which measures the same economic output from the income side — grew 1.2% in Q1, revised up from 0.9% but still well below the 2.1% GDP headline. The average of GDP and GDI — the BEA's preferred composite — was 1.7%. That figure is the more honest answer to "how fast did the economy grow in Q1?" It's also the number that aligns with the private domestic demand reading.

The structure of an economy where the income side reports 1.2% growth while the spending side reports 2.1% is an economy where consumers are outspending what they're earning. How that gap is financed is the May PCE story.

May PCE: 4.1%, the highest in three years

The May Personal Income and Outlays report contains the Federal Reserve's preferred inflation measure. In May, the PCE price index rose 4.1% year-over-year. Core PCE — excluding food and energy — rose 3.4% year-over-year. Both are three-year highs. Both are more than double the Fed's 2% target.

The acceleration from April to May is modest — 3.8% to 4.1% headline, 3.3% to 3.4% core — but the direction matters as much as the increment. The PCE price index within Q1 GDP (the quarter-level measure) was revised up to 4.6% annualized in the third estimate, versus 4.5% in the second estimate. The monthly and quarterly data are consistent: inflation moved higher in Q1 and continued higher into May.

Personal income grew 0.7% in May — a better month than April's 0.0% — primarily driven by farm proprietors' income from USDA disaster relief payments under the American Relief Act of 2025. Strip out the one-time government transfer and income growth was more modest. Real disposable personal income — adjusted for inflation — grew 0.3% in May after falling 0.5% in April.

The personal saving rate was 3.0% in May, unchanged from April, and down from 4.9% in May 2025. The long-run average from 1959 to the present is approximately 8.4%. The all-time low was 1.4% in July 2005. The current reading sits roughly halfway between that low and historical normal — sustainable in the near term, but without the buffer that households would need to absorb an income shock or another leg of inflation.

The household debt context adds pressure. Total U.S. household debt reached a record $18.79 trillion in Q1 2026, according to the New York Federal Reserve. Mortgage balances ($13.19T), auto loans ($1.68T), and home equity lines of credit ($446B) all grew. Credit card balances fell slightly — but new bankcard originations surged 8.1% through January 2026, with subprime originations up 18.6%. The delinquency rate held at 4.8% of outstanding debt. The picture is of a consumer sector using a combination of savings drawdown, new credit, and balance sheet leverage to sustain spending that income growth alone doesn't support.

What this does to the rate picture

The June 16-17 FOMC meeting — Kevin Warsh's first as chair — held rates at 3.50-3.75%. The dot plot shifted: nine of nineteen officials projected at least one rate hike by year-end, against eight projecting no change and one projecting a cut. Warsh declined to submit his own dot, consistent with his stated view that the Fed should react to real-time data rather than manage markets through forward guidance.

The June 25 data is the real-time data the next FOMC meeting will read. As of June 25, market pricing placed 80% probability on at least one 25-basis-point hike by year-end, with 40% probability of two or more. Those probabilities moved after the PCE release.

The position is straightforward: PCE at 4.1% is 2.1 percentage points above target. The Fed has not cut rates in this cycle. The dot plot now implies a hike is more likely than not. The May data does not provide the deceleration in inflation that would change that calculation. PNC Bank economists, reacting to the release, projected no change in the fed funds rate through 2026 and into 2027. Gus Faucher of PNC Financial Services Group projected a consumer spending slowdown in the second half of 2026 and into 2027 as inflation erodes purchasing power and job growth moderates.

Kathy Bostjancic of Nationwide expressed more optimism — arguing that inflation has likely peaked and should cool in the second half, allowing the Fed to hold steady through 2027 rather than hike. That view requires May's 4.1% to be the high-water mark. The June CPI (releasing July 10) and June PCE (releasing July 30) will test that assumption.

The AI capital cost connection

The relevance of the rate picture for AI infrastructure finance is not abstract. As covered here on June 22, the hyperscalers — Microsoft, Amazon, Alphabet, Meta — committed $630-$725 billion in AI capex in a week that coincided with the FOMC dot plot's hawkish pivot. Their financing does not depend on the Fed; their balance sheets are effectively self-funding.

The broader AI infrastructure ecosystem does not have that luxury. Data center construction loans, private credit facilities backing compute buildouts, cloud-adjacent companies financing GPU clusters on investment-grade or high-yield terms: all of this is priced against the risk-free rate that Warsh's FOMC will set. Investment-grade AI debt in this environment carries coupons of 4-4.5%; high-yield is 7-9%. Private credit adds 50-100 basis points above syndicated rates. Every 25 basis points of tightening adds approximately $1.25 billion per year in annual interest cost on $500 billion of financed AI capex.

If inflation remains at 4.1% and the FOMC delivers one hike by year-end — the modal market expectation as of this release — the capital cost assumption embedded in AI buildout pro formas from six months ago is wrong. Not catastrophically wrong for the hyperscalers. Materially wrong for the financing-dependent players.

The sentence the coverage used and the sentence it should have

The June 25 GDP revision produced a wave of coverage summarized by some version of: "U.S. economy grew 2.1% in Q1, better than expected." The sentence is accurate and misleading simultaneously. It accurately reports the BEA headline. It misleads by implying the revision reflects stronger economic conditions.

The more accurate sentence: "Q1 GDP was revised up to 2.1%, driven by a downward import revision, while consumer spending growth — revised to 0.5%, the slowest in four years — and private domestic demand were both downgraded. Simultaneously, May PCE inflation hit a three-year high of 4.1%."

That is a longer sentence. It is also the economy.

The June jobs report releases Thursday, July 2. June CPI: July 10. The next FOMC meeting is scheduled for July 28-29.

Correction policy: Offworld News AI corrects errors promptly and transparently. If you find a factual error in this piece, contact us at editor@offworldnews.ai.

Sources

- Bureau of Economic Analysis. "GDP (Third Estimate), Industries, Corporate Profits, State GDP, and State Personal Income, 1st Quarter 2026." June 25, 2026. <https://www.bea.gov/news/2026/gdp-third-estimate-industries-corporate-profits-state-gdp-and-state-personal-income-1st>

- Bureau of Economic Analysis. "Personal Income and Outlays, May 2026." June 25, 2026. <https://www.bea.gov/news/2026/personal-income-and-outlays-may-2026>

- Bureau of Economic Analysis. "Personal Saving Rate." Historical series. <https://www.bea.gov/data/income-saving/personal-saving-rate>

- Haver Analytics. "Unusually Large Upward Revision in Third Estimate of U.S. Q1 2026 Real GDP Growth." June 25, 2026. <https://www.haver.com/articles/unusually-large-upward-revision-in-third-estimate-of-u-s-q1-2026-real-gdp-growth>

- American Bankers Association. "ABA DataBank: Q1 GDP Revised Up." June 25, 2026. <https://bankingjournal.aba.com/2026/06/aba-databank-q1-gdp-revised-up/>

- Federal Reserve. FOMC Press Conference, June 17, 2026. <https://www.federalreserve.gov/monetarypolicy/fomcpresconf20260617.htm>

- Federal Reserve Bank of New York. "Household Debt and Credit Report, Q1 2026." May 12, 2026. <https://www.newyorkfed.org/newsevents/news/research/2026/20260512>

- Pittsburgh Post-Gazette / PNC Financial Services Group. "Economists view consumer spending." June 29, 2026. <https://www.post-gazette.com/business/money/2026/06/29/economists-view-consumer-spending-pnc-gus-faucher/stories/202606280050>

- Trading Economics. "United States Personal Savings Rate." Historical series. <https://tradingeconomics.com/united-states/personal-savings>